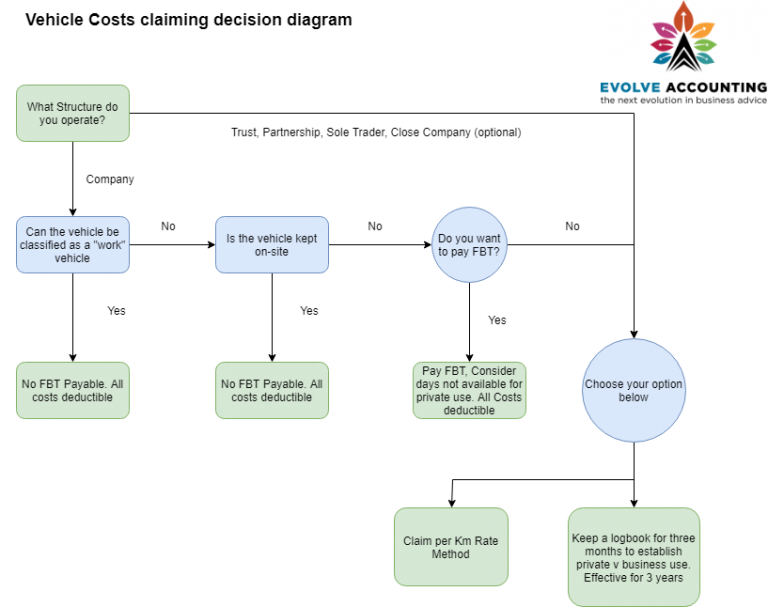

The scenarios around claiming motor vehicle costs for small business is perhaps one of the most common questions we get asked. It's not all that surprising when you consider the multitude of options available in conjunction with the implications of getting it wrong. Getting it wrong can include not claiming these costs as a valid business expense or being hit with an unexpected tax bill for taking the wrong approach. At the bottom of this article is a handy diagram that will also help you wade through the options available.

The options available can be distilled into the following 4 options:

For all options it must be remembered that travel to and from a fixed place of work (i.e. office) is considered personal travel.

1. Per km rate reimbursement

If you own the vehicle personally, you can be reimbursed for business use on a per km rate. Unfortunately from the 2018 tax year the calculation of this got a bit more complicated but an improvement was provided to sole traders who has previously been restricted to claiming the rate on a maximum of 5,000km.

Points to note about using this rate:

- This method reduces the business usage to 25% should you not be able to produce the logbook upon IRD's request

- Once this method is chosen you must apply it each year until the vehicle is disposed. You can't change methods.

- It allow for unlimited kms to be claimed if a full logbook is kept using the rates below

- A vehicle logbook must be kept for at least 3 months to establish the business proportion (valid for 3 years after that)

- An initial odometer reading needs to be done and then at the end of 31 March each year to determine the total km's travelled in the year

Thee rates set by the IRD each year take into account not only the petrol costs associated with running a vehicle but also wear and tear and expected maintenance costs. There is no tax to pay if the vehicle is sold

| Vehicle Type | (Tier 1) First 14,000 kms | (Tier 2) After 14,000 kms |

| Petrol | $1.17 | 37 cents |

| Diesel | $1.26 | 35 cents |

| Petrol hybrid | $0.86 | 21 cents |

| Electric | $1.08 | 19 cents |

The rates mentioned above are effective for the 2025 year onwards.

Business Usage = Total Business KM / Total KM (obtained from keeping logbook for 3 months)

Per KM rate reimbursement = (Tier 1 Km rate X Business Usage) + (Tier 2 km Rate x Business Usage)

| Pros |

|

| Cons |

|

2. Private Ownership - Claim % of Actual Costs

Maintain a vehicle log book for 3 months to establish the business usage of a private vehicle will determine what % of actual costs can be claimed for income tax purposes. The business % established can be used for 3 years after this date.

| Pros |

|

| Cons |

|

3. Business Ownership - Claim % of Costs

Again in this scenario, a vehicle log book is maintained. The difference in the business ownership scenario is that a claim for GST purposes can be made on the purchase of the vehicle. However, an increased level of compliance occurs with GST calculations if down the track the % of business usage changes.

| Pros |

|

| Cons |

|

Logbooks

Options 1 - 3 require a vehicle logbook to be kept for at least three months to establish the business usage. In terms of vehicle log books there are the obvious paper-based log books which can be purchased from a local stationary outlet, however, there are also a number of apps for mobile phone which capture your trips when they connect to your vehicles Bluetooth, reducing the amount of administration that is otherwise required.

4. Company Ownership - FBT

If a vehicle is owned in a company, and you don't want to maintain a log book then it is likely the vehicle will be subject to the Fringe Benefit Tax (FBT) rules. This is a tax levied on the cost value of the vehicle and based on it's "availability"* for private use. On the flip side, all costs associated with the vehicle are deductible. A cost-benefit analysis needs to be considered in conjunction with a number of other matters with this method and as such should be done in conjunction with discussions with your accountant. Generally the higher value the vehicle is the less likely this method will provide a net benefit to you.

There are a number of ways to minimise FBT if you meet certain criteria.

These are:

A) Putting in place restrictive use arrangement of owner-employees:

- A vehicle of any type that has a restriction placed by the company upon the employee that the vehicle is only to be used for business purposes (often done by way of a letter from the company to the employee).

- Maintain a log-book for 3 months to show that there was no private usage, and/or quarterly checks with the employee

- Evidence that the employee has another vehicle that is used for private related travel

B) Meeting the work vehicle exemptions, which involves meeting ALL of the following criteria:

- The vehicle is not designed for carrying passengers (No sedans, hatchbacks, SUV's) and weighs less than 3,500kg. (basically a van or a ute)

- It has prominent sign writing that can't be easily removed

- There is written documentation between company and employee that the vehicle can only be used for business purposes and the small private element that exists that is the travel between home and work. Furthermore this arrangement should be checked by the company against the employee every few months

The options above to minimise the impact of FBT applying require a level of administration in themselves and are not a case of set and forget.

| Pros |

|

| Cons |

|

* "Availability" for private use is not about whether it is actually used on a given day for private purposes, but whether an employee has access (i.e. has possession of the vehicle) and is given permission to use the vehicle (or the lack of a letter restricting the use of the vehicle for only business purposes between the company and the employee).